" width="90.99999664790107px"><path d="M 3.854 4.052 C 3.633 4.251 3.308 4.259 3.064 4.087 C 2.845 3.933 2.585 3.856 2.285 3.856 C 2.092 3.856 1.904 3.905 1.72 4.001 C 1.535 4.097 1.443 4.255 1.443 4.472 C 1.443 4.649 1.519 4.779 1.671 4.859 C 1.824 4.94 2.016 5.009 2.249 5.065 C 2.482 5.122 2.732 5.179 3.001 5.24 C 3.27 5.301 3.521 5.393 3.753 5.518 C 3.986 5.643 4.179 5.814 4.331 6.031 C 4.484 6.249 4.559 6.547 4.559 6.926 C 4.559 7.272 4.485 7.564 4.337 7.801 C 4.188 8.039 3.996 8.23 3.759 8.375 C 3.522 8.52 3.256 8.625 2.959 8.69 C 2.663 8.754 2.366 8.786 2.069 8.786 C 1.612 8.786 1.198 8.722 0.824 8.593 C 0.687 8.546 0.556 8.484 0.43 8.409 C 0.075 8.197 0.023 7.7 0.325 7.417 L 0.357 7.387 C 0.581 7.176 0.925 7.162 1.167 7.352 C 1.236 7.405 1.306 7.455 1.377 7.5 C 1.59 7.633 1.848 7.699 2.153 7.699 C 2.257 7.699 2.366 7.687 2.478 7.662 C 2.59 7.638 2.694 7.598 2.791 7.541 C 2.887 7.485 2.966 7.414 3.026 7.329 C 3.086 7.245 3.116 7.146 3.116 7.033 C 3.116 6.832 3.04 6.683 2.888 6.585 C 2.736 6.489 2.543 6.41 2.31 6.35 C 2.077 6.289 1.827 6.233 1.558 6.181 C 1.29 6.129 1.039 6.044 0.806 5.927 C 0.577 5.813 0.378 5.645 0.228 5.437 C 0.076 5.228 0 4.937 0 4.567 C 0 4.245 0.066 3.964 0.198 3.727 C 0.33 3.489 0.505 3.294 0.721 3.141 C 0.937 2.988 1.186 2.875 1.467 2.802 C 1.747 2.73 2.032 2.693 2.321 2.693 C 2.706 2.693 3.087 2.759 3.464 2.892 C 3.568 2.929 3.666 2.973 3.759 3.023 C 4.133 3.229 4.188 3.748 3.871 4.034 L 3.855 4.049 Z M 5.851 2.84 L 5.958 2.84 C 6.255 2.84 6.519 3.035 6.607 3.321 L 7.709 6.9 L 7.733 6.9 L 8.758 3.333 C 8.842 3.041 9.108 2.84 9.411 2.84 L 9.962 2.84 C 10.259 2.84 10.523 3.035 10.611 3.321 L 11.714 6.9 L 11.737 6.9 L 12.795 3.328 C 12.881 3.038 13.146 2.84 13.447 2.84 C 13.912 2.84 14.24 3.3 14.09 3.742 L 12.592 8.177 C 12.498 8.454 12.239 8.64 11.948 8.64 L 11.487 8.64 C 11.198 8.64 10.94 8.456 10.845 8.182 L 9.633 4.677 L 9.61 4.677 L 8.543 8.159 C 8.455 8.445 8.191 8.641 7.893 8.64 L 7.386 8.64 C 7.097 8.64 6.839 8.456 6.744 8.182 L 5.209 3.747 C 5.056 3.303 5.383 2.84 5.851 2.84 Z M 18.859 7.843 L 18.822 7.843 C 18.613 8.182 18.349 8.424 18.028 8.569 C 17.708 8.714 17.354 8.786 16.969 8.786 C 16.705 8.786 16.446 8.75 16.193 8.677 C 15.941 8.605 15.716 8.496 15.52 8.351 C 15.324 8.206 15.162 8.021 15.044 7.807 C 14.924 7.589 14.863 7.335 14.863 7.046 C 14.863 6.731 14.919 6.463 15.031 6.242 C 15.144 6.02 15.294 5.835 15.482 5.687 C 15.67 5.538 15.889 5.419 16.138 5.33 C 16.386 5.241 16.645 5.175 16.914 5.131 C 17.182 5.087 17.453 5.058 17.725 5.046 C 17.998 5.035 18.254 5.028 18.494 5.028 L 18.699 5.028 C 18.786 5.028 18.855 4.958 18.855 4.871 C 18.855 4.509 18.731 4.237 18.483 4.056 C 18.234 3.875 17.918 3.784 17.532 3.784 C 17.228 3.784 16.943 3.838 16.678 3.947 C 16.551 3.999 16.433 4.06 16.323 4.129 C 16.11 4.264 15.832 4.228 15.655 4.049 C 15.411 3.804 15.449 3.393 15.738 3.205 C 15.931 3.079 16.138 2.98 16.36 2.908 C 16.788 2.767 17.237 2.695 17.688 2.696 C 18.097 2.696 18.442 2.743 18.723 2.836 C 19.003 2.928 19.236 3.047 19.42 3.192 C 19.604 3.337 19.747 3.505 19.847 3.694 C 19.948 3.884 20.02 4.074 20.064 4.268 C 20.107 4.461 20.134 4.648 20.142 4.83 C 20.15 5.012 20.154 5.17 20.154 5.308 L 20.154 7.99 C 20.154 8.351 19.863 8.643 19.504 8.643 C 19.145 8.643 18.854 8.351 18.854 7.99 L 18.854 7.845 Z M 18.775 6.2 C 18.775 6.113 18.704 6.043 18.619 6.043 L 18.474 6.043 C 18.274 6.043 18.049 6.052 17.801 6.067 C 17.552 6.084 17.318 6.121 17.097 6.182 C 16.876 6.242 16.69 6.333 16.537 6.453 C 16.385 6.574 16.309 6.736 16.309 6.937 C 16.309 7.073 16.339 7.189 16.4 7.281 C 16.461 7.375 16.541 7.455 16.634 7.517 C 16.73 7.581 16.839 7.628 16.959 7.656 C 17.08 7.685 17.2 7.699 17.32 7.699 C 17.824 7.699 18.193 7.58 18.426 7.342 C 18.659 7.104 18.775 6.78 18.775 6.369 L 18.775 6.199 Z M 22.431 2.84 C 22.83 2.84 23.153 3.165 23.153 3.565 L 23.153 3.759 L 23.177 3.759 C 23.338 3.421 23.566 3.159 23.862 2.973 C 24.159 2.788 24.5 2.695 24.885 2.695 C 24.973 2.695 25.059 2.703 25.143 2.719 L 25.146 2.719 C 25.295 2.748 25.402 2.881 25.402 3.034 L 25.402 3.802 C 25.402 3.991 25.232 4.134 25.047 4.102 C 24.931 4.082 24.816 4.072 24.704 4.072 C 24.367 4.072 24.097 4.134 23.893 4.259 C 23.688 4.383 23.532 4.527 23.423 4.688 C 23.315 4.849 23.243 5.01 23.207 5.171 C 23.171 5.333 23.153 5.454 23.153 5.533 L 23.153 7.914 C 23.153 8.315 22.83 8.639 22.431 8.639 C 22.032 8.639 21.709 8.315 21.709 7.914 L 21.709 3.564 C 21.709 3.163 22.032 2.838 22.431 2.838 Z M 27.23 2.84 C 27.608 2.84 27.915 3.148 27.915 3.529 L 27.915 3.746 L 27.939 3.746 C 28.067 3.472 28.274 3.229 28.559 3.015 C 28.843 2.802 29.226 2.695 29.707 2.695 C 30.298 2.695 30.761 2.851 31.095 3.162 C 31.348 3.398 31.735 3.387 31.997 3.162 C 32.088 3.083 32.187 3.014 32.293 2.956 C 32.606 2.782 32.978 2.696 33.412 2.696 C 33.797 2.696 34.121 2.76 34.386 2.89 C 34.65 3.019 34.865 3.196 35.029 3.421 C 35.194 3.647 35.312 3.911 35.384 4.213 C 35.456 4.515 35.493 4.839 35.493 5.186 L 35.493 7.954 C 35.493 8.334 35.186 8.642 34.807 8.642 L 34.735 8.642 C 34.357 8.642 34.05 8.334 34.05 7.954 L 34.05 5.356 C 34.05 5.179 34.033 5.007 34.001 4.842 C 33.969 4.677 33.913 4.532 33.833 4.407 C 33.753 4.283 33.645 4.184 33.509 4.111 C 33.373 4.039 33.195 4.002 32.979 4.002 C 32.763 4.002 32.564 4.044 32.408 4.129 C 32.252 4.213 32.123 4.326 32.023 4.467 C 31.922 4.608 31.85 4.769 31.806 4.95 C 31.763 5.13 31.741 5.315 31.741 5.5 L 31.741 7.954 C 31.741 8.334 31.434 8.642 31.055 8.642 L 30.983 8.642 C 30.604 8.642 30.297 8.334 30.297 7.954 L 30.297 5.186 C 30.297 4.824 30.223 4.536 30.075 4.322 C 29.926 4.108 29.672 4.002 29.311 4.002 C 29.07 4.002 28.868 4.042 28.704 4.123 C 28.539 4.204 28.403 4.313 28.295 4.449 C 28.186 4.586 28.109 4.744 28.06 4.921 C 28.012 5.098 27.988 5.283 27.988 5.477 L 27.988 7.954 C 27.988 8.334 27.681 8.642 27.303 8.642 L 27.231 8.642 C 26.852 8.642 26.545 8.334 26.545 7.954 L 26.545 3.531 C 26.545 3.15 26.852 2.842 27.231 2.842 Z M 36.888 0.871 C 36.888 0.637 36.973 0.435 37.146 0.261 C 37.318 0.088 37.537 0.002 37.801 0.002 C 38.066 0.002 38.289 0.084 38.469 0.249 C 38.649 0.415 38.739 0.622 38.739 0.872 C 38.739 1.122 38.648 1.33 38.469 1.495 C 38.288 1.66 38.066 1.742 37.801 1.742 C 37.537 1.742 37.318 1.656 37.146 1.483 C 36.973 1.31 36.888 1.106 36.888 0.873 Z M 37.814 2.84 C 38.213 2.84 38.536 3.165 38.536 3.565 L 38.536 7.916 C 38.536 8.317 38.213 8.641 37.814 8.641 C 37.415 8.641 37.092 8.317 37.092 7.916 L 37.092 3.565 C 37.092 3.165 37.415 2.84 37.814 2.84 Z M 39.907 5.741 C 39.907 5.281 39.989 4.865 40.153 4.49 C 40.318 4.116 40.54 3.795 40.821 3.529 C 41.101 3.263 41.434 3.057 41.819 2.913 C 42.204 2.768 42.613 2.695 43.046 2.695 C 43.479 2.695 43.888 2.768 44.273 2.913 C 44.658 3.057 44.99 3.263 45.271 3.529 C 45.552 3.795 45.774 4.115 45.939 4.49 C 46.103 4.864 46.185 5.281 46.185 5.741 C 46.185 6.2 46.103 6.616 45.939 6.992 C 45.774 7.366 45.552 7.687 45.271 7.953 C 44.99 8.219 44.658 8.424 44.273 8.569 C 43.888 8.714 43.479 8.786 43.046 8.786 C 42.613 8.786 42.204 8.714 41.819 8.569 C 41.434 8.424 41.102 8.219 40.821 7.953 C 40.54 7.687 40.318 7.367 40.153 6.992 C 39.989 6.617 39.907 6.2 39.907 5.741 Z M 41.35 5.741 C 41.35 5.966 41.388 6.184 41.464 6.394 C 41.54 6.604 41.652 6.789 41.801 6.949 C 41.949 7.111 42.128 7.239 42.336 7.336 C 42.544 7.433 42.781 7.481 43.045 7.481 C 43.309 7.481 43.546 7.433 43.754 7.336 C 43.962 7.24 44.141 7.111 44.289 6.949 C 44.437 6.788 44.551 6.599 44.626 6.394 C 44.702 6.185 44.74 5.966 44.74 5.741 C 44.74 5.515 44.702 5.298 44.626 5.088 C 44.549 4.879 44.438 4.693 44.289 4.532 C 44.14 4.371 43.962 4.242 43.754 4.145 C 43.545 4.049 43.309 4 43.045 4 C 42.781 4 42.544 4.049 42.336 4.145 C 42.127 4.241 41.949 4.371 41.801 4.532 C 41.653 4.693 41.538 4.882 41.464 5.088 C 41.388 5.298 41.35 5.515 41.35 5.741 Z M 49.11 0.875 C 49.11 0.64 49.197 0.436 49.371 0.261 C 49.544 0.087 49.763 0 50.03 0 C 50.296 0 50.519 0.083 50.7 0.249 C 50.882 0.415 50.972 0.624 50.972 0.874 C 50.972 1.124 50.882 1.333 50.7 1.499 C 50.519 1.665 50.295 1.748 50.03 1.748 C 49.764 1.748 49.544 1.661 49.371 1.487 C 49.197 1.312 49.11 1.108 49.11 0.873 Z M 65.441 7.481 C 65.441 7.246 65.527 7.042 65.701 6.868 C 65.874 6.694 66.093 6.606 66.36 6.606 C 66.626 6.606 66.849 6.69 67.031 6.855 C 67.212 7.021 67.303 7.23 67.303 7.48 C 67.303 7.731 67.212 7.94 67.031 8.106 C 66.849 8.272 66.626 8.354 66.36 8.354 C 66.094 8.354 65.874 8.267 65.701 8.093 C 65.527 7.919 65.441 7.714 65.441 7.479 Z M 50.041 2.855 C 50.442 2.855 50.767 3.181 50.767 3.584 L 50.767 7.956 C 50.767 8.359 50.442 8.685 50.041 8.685 C 49.641 8.685 49.316 8.359 49.316 7.956 L 49.316 3.584 C 49.316 3.181 49.641 2.855 50.041 2.855 Z M 53.124 2.855 C 53.504 2.855 53.813 3.165 53.813 3.547 L 53.813 3.79 L 53.837 3.79 C 53.974 3.499 54.184 3.245 54.466 3.031 C 54.748 2.816 55.13 2.709 55.614 2.709 C 56.001 2.709 56.329 2.774 56.599 2.903 C 56.869 3.033 57.088 3.203 57.258 3.413 C 57.427 3.624 57.548 3.867 57.62 4.142 C 57.692 4.417 57.729 4.705 57.729 5.004 L 57.729 7.992 C 57.729 8.374 57.42 8.684 57.04 8.684 L 56.968 8.684 C 56.587 8.684 56.278 8.374 56.278 7.992 L 56.278 5.733 C 56.278 5.571 56.27 5.391 56.255 5.193 C 56.238 4.995 56.196 4.809 56.128 4.635 C 56.059 4.461 55.953 4.315 55.807 4.197 C 55.662 4.08 55.465 4.021 55.215 4.021 C 54.965 4.021 54.77 4.062 54.604 4.142 C 54.439 4.223 54.302 4.333 54.194 4.471 C 54.085 4.608 54.007 4.766 53.958 4.945 C 53.91 5.123 53.886 5.309 53.886 5.503 L 53.886 7.993 C 53.886 8.375 53.577 8.685 53.197 8.685 L 53.125 8.685 C 52.744 8.685 52.436 8.375 52.436 7.993 L 52.436 3.548 C 52.436 3.166 52.744 2.856 53.125 2.856 Z M 63.882 4.059 C 63.606 4.335 63.182 4.393 62.843 4.2 L 62.806 4.179 C 62.621 4.074 62.431 4.021 62.238 4.021 C 61.972 4.021 61.734 4.07 61.525 4.167 C 61.315 4.264 61.136 4.394 60.987 4.556 C 60.838 4.718 60.725 4.904 60.649 5.114 C 60.572 5.325 60.534 5.544 60.534 5.77 C 60.534 5.997 60.572 6.216 60.649 6.426 C 60.725 6.637 60.838 6.823 60.987 6.984 C 61.136 7.147 61.316 7.276 61.525 7.373 C 61.734 7.47 61.972 7.519 62.238 7.519 C 62.477 7.519 62.693 7.469 62.887 7.37 C 63.229 7.195 63.646 7.279 63.908 7.561 L 63.952 7.609 C 64.174 7.849 64.113 8.234 63.828 8.393 C 63.638 8.498 63.447 8.584 63.254 8.648 C 63.06 8.713 62.875 8.759 62.698 8.787 C 62.521 8.816 62.367 8.829 62.239 8.829 C 61.803 8.829 61.393 8.757 61.006 8.611 C 60.619 8.465 60.285 8.259 60.002 7.992 C 59.72 7.725 59.497 7.403 59.332 7.026 C 59.166 6.649 59.083 6.23 59.083 5.769 C 59.083 5.308 59.165 4.889 59.332 4.512 C 59.497 4.135 59.72 3.813 60.002 3.546 C 60.285 3.279 60.619 3.072 61.006 2.927 C 61.393 2.781 61.803 2.709 62.239 2.709 C 62.609 2.709 62.983 2.78 63.357 2.922 C 63.504 2.978 63.644 3.046 63.777 3.127 C 64.104 3.327 64.152 3.786 63.882 4.059 Z" fill="rgb(7, 7, 145)" height="8.82930526882696px" id="ikZ9oAiXW" transform="translate(23.697 4.13)" width="67.30277679926826px"/><path d="M 7.419 19.65 L 7.389 19.65 C 7.361 19.642 7.331 19.634 7.303 19.624 C 6.8 19.451 6.298 19.277 5.795 19.105 C 5.549 19.022 5.329 18.899 5.154 18.701 C 4.851 18.358 4.509 18.06 4.136 17.796 C 3.943 17.659 3.751 17.521 3.584 17.354 C 3.23 17.003 2.839 16.702 2.405 16.458 C 2.216 16.352 2.048 16.215 1.907 16.05 C 1.65 15.752 1.437 15.424 1.234 15.088 C 1.063 14.806 0.899 14.519 0.812 14.197 C 0.745 13.946 0.69 13.69 0.642 13.434 C 0.58 13.109 0.528 12.782 0.476 12.455 C 0.434 12.197 0.394 11.938 0.363 11.68 C 0.334 11.442 0.311 11.204 0.298 10.965 C 0.283 10.708 0.309 10.454 0.403 10.21 C 0.524 9.892 0.719 9.625 0.949 9.381 C 1.224 9.089 1.433 8.756 1.52 8.364 C 1.585 8.07 1.616 7.77 1.658 7.471 C 1.688 7.268 1.701 7.062 1.74 6.86 C 1.873 6.157 2.22 5.579 2.775 5.131 C 3.126 4.848 3.487 4.575 3.843 4.297 C 4.324 3.919 4.682 3.451 4.882 2.867 C 4.945 2.684 5.003 2.497 4.997 2.299 C 4.993 2.117 4.896 2.001 4.717 1.987 C 4.622 1.978 4.522 1.98 4.43 2.003 C 4.192 2.061 3.958 2.133 3.722 2.199 C 3.538 2.251 3.354 2.302 3.168 2.352 C 3.149 2.357 3.12 2.355 3.106 2.343 C 3.08 2.321 3.108 2.299 3.119 2.279 C 3.157 2.204 3.216 2.149 3.28 2.097 C 3.642 1.809 4.001 1.519 4.362 1.232 C 4.653 1.001 4.99 0.955 5.347 0.988 C 5.551 1.007 5.757 1.027 5.96 0.991 C 6.401 0.913 6.842 0.83 7.282 0.747 C 7.514 0.703 7.745 0.685 7.976 0.749 C 8.266 0.828 8.471 1.016 8.644 1.257 C 8.789 1.459 8.941 1.658 9.103 1.847 C 9.352 2.138 9.652 2.362 10.02 2.48 C 10.316 2.574 10.623 2.624 10.932 2.647 C 11.252 2.671 11.569 2.657 11.882 2.585 C 12.132 2.528 12.373 2.443 12.593 2.31 C 12.724 2.231 12.819 2.122 12.852 1.967 C 12.877 1.848 12.859 1.731 12.83 1.614 C 12.783 1.427 12.73 1.243 12.691 1.055 C 12.645 0.83 12.751 0.681 12.975 0.642 C 13.039 0.631 13.104 0.619 13.168 0.617 C 13.308 0.614 13.451 0.597 13.587 0.623 C 13.76 0.656 13.931 0.716 14.096 0.78 C 14.643 0.993 15.14 1.295 15.615 1.636 C 15.925 1.859 16.094 2.17 16.165 2.54 C 16.193 2.687 16.119 2.79 15.97 2.823 C 15.926 2.832 15.881 2.839 15.836 2.841 C 15.56 2.859 15.283 2.872 15.008 2.894 C 14.84 2.907 14.675 2.94 14.517 3.005 C 14.212 3.127 14.026 3.347 13.994 3.68 C 13.969 3.934 13.998 4.181 14.071 4.425 C 14.392 5.492 15.089 6.161 16.163 6.434 C 16.37 6.487 16.58 6.524 16.784 6.587 C 17.108 6.687 17.395 6.857 17.63 7.106 C 17.966 7.46 18.123 7.895 18.192 8.369 C 18.217 8.534 18.232 8.702 18.264 8.866 C 18.334 9.213 18.51 9.489 18.82 9.671 C 18.892 9.713 18.963 9.759 19.031 9.806 C 19.243 9.954 19.4 10.148 19.51 10.382 C 19.602 10.577 19.638 10.787 19.689 10.992 C 19.729 11.15 19.725 11.309 19.713 11.467 C 19.702 11.613 19.658 11.756 19.627 11.899 C 19.49 12.531 19.184 13.043 18.637 13.411 C 18.006 13.834 17.654 14.443 17.545 15.193 C 17.484 15.616 17.329 15.993 17.047 16.314 C 16.856 16.531 16.63 16.706 16.388 16.859 C 15.92 17.155 15.564 17.545 15.336 18.054 C 15.176 18.415 14.913 18.678 14.549 18.833 C 14.194 18.984 13.837 19.134 13.479 19.28 C 13.251 19.373 13.019 19.458 12.787 19.544 C 12.593 19.617 12.389 19.618 12.185 19.62 C 12.023 19.62 11.872 19.584 11.736 19.499 C 11.62 19.425 11.505 19.344 11.394 19.262 C 11.114 19.055 10.805 18.94 10.454 18.948 C 10.192 18.955 9.929 18.959 9.668 18.953 C 9.497 18.948 9.325 18.934 9.157 18.902 C 8.747 18.826 8.413 18.623 8.185 18.263 C 7.957 17.904 7.93 17.531 8.138 17.155 C 8.289 16.885 8.532 16.735 8.828 16.665 C 9.197 16.577 9.57 16.561 9.946 16.603 C 10.268 16.639 10.568 16.736 10.842 16.911 C 11.161 17.115 11.39 17.4 11.572 17.73 C 11.662 17.894 11.761 18.054 11.869 18.207 C 11.989 18.379 12.157 18.473 12.374 18.458 C 12.526 18.447 12.677 18.441 12.829 18.427 C 13.136 18.399 13.434 18.329 13.72 18.214 C 14.164 18.034 14.515 17.744 14.732 17.308 C 14.864 17.042 14.959 16.76 15.031 16.473 C 15.143 16.029 15.351 15.644 15.679 15.326 C 15.919 15.094 16.192 14.906 16.474 14.733 C 16.748 14.564 17.005 14.372 17.232 14.143 C 17.639 13.73 17.918 13.242 18.074 12.684 C 18.163 12.365 18.232 12.04 18.219 11.705 C 18.206 11.397 18.081 11.142 17.841 10.948 C 17.52 10.688 17.17 10.629 16.798 10.823 C 16.674 10.887 16.558 10.97 16.447 11.055 C 16.03 11.379 15.699 11.773 15.51 12.274 C 15.351 12.695 15.262 13.135 15.198 13.58 C 15.148 13.917 15.055 14.24 14.894 14.541 C 14.633 15.025 14.249 15.388 13.782 15.665 C 13.323 15.936 12.834 15.997 12.321 15.854 C 11.767 15.699 11.377 15.362 11.179 14.814 C 11.109 14.621 11.061 14.42 11.002 14.224 C 10.877 13.814 10.666 13.456 10.344 13.173 C 9.742 12.64 9.039 12.439 8.247 12.552 C 7.887 12.603 7.558 12.733 7.265 12.951 C 6.681 13.386 6.405 14.052 6.647 14.805 C 6.756 15.146 6.762 15.497 6.706 15.85 C 6.681 16.008 6.618 16.151 6.494 16.261 C 6.361 16.381 6.2 16.418 6.027 16.421 C 5.832 16.425 5.637 16.43 5.442 16.44 C 5.3 16.448 5.166 16.49 5.051 16.578 C 4.818 16.756 4.721 17.091 4.81 17.399 C 4.875 17.622 5.013 17.797 5.17 17.96 C 5.443 18.242 5.78 18.418 6.148 18.538 C 6.457 18.639 6.768 18.734 7.078 18.831 C 7.288 18.897 7.477 18.997 7.634 19.157 C 7.721 19.245 7.749 19.346 7.74 19.464 C 7.733 19.558 7.706 19.588 7.612 19.611 C 7.549 19.626 7.487 19.64 7.423 19.654 Z M 15.071 9.45 C 15.065 9.185 15.044 8.949 14.999 8.715 C 14.871 8.038 14.518 7.506 13.957 7.118 C 13.446 6.766 12.875 6.654 12.265 6.748 C 11.813 6.817 11.405 6.994 11.075 7.311 C 10.401 7.958 10.108 8.748 10.254 9.682 C 10.343 10.256 10.595 10.755 11.019 11.156 C 11.416 11.533 11.891 11.75 12.435 11.806 C 12.759 11.839 13.074 11.792 13.378 11.681 C 13.939 11.477 14.371 11.11 14.693 10.611 C 14.926 10.251 15.077 9.862 15.072 9.45 Z M 7.52 3.164 C 7.382 3.177 7.245 3.186 7.108 3.204 C 6.735 3.255 6.391 3.386 6.077 3.594 C 5.635 3.887 5.313 4.286 5.062 4.747 C 4.909 5.029 4.808 5.329 4.783 5.652 C 4.757 5.99 4.822 6.313 4.971 6.618 C 5.306 7.303 5.856 7.652 6.614 7.67 C 6.889 7.677 7.16 7.639 7.425 7.57 C 8.104 7.394 8.669 7.042 9.071 6.458 C 9.433 5.932 9.595 5.349 9.484 4.71 C 9.401 4.237 9.162 3.855 8.778 3.569 C 8.406 3.292 7.981 3.172 7.52 3.165 Z M 1.965 10.5 C 1.97 10.705 1.994 10.931 2.045 11.154 C 2.21 11.89 2.604 12.454 3.275 12.809 C 3.588 12.975 3.919 13.05 4.27 12.982 C 4.739 12.892 5.075 12.621 5.296 12.199 C 5.401 11.998 5.457 11.781 5.496 11.56 C 5.521 11.416 5.572 11.273 5.554 11.124 C 5.529 10.913 5.507 10.701 5.465 10.493 C 5.355 9.949 5.117 9.472 4.717 9.082 C 4.35 8.724 3.915 8.551 3.403 8.613 C 3.007 8.662 2.68 8.851 2.423 9.156 C 2.104 9.537 1.971 9.984 1.965 10.499 Z M 3.528 15.472 C 3.518 15.392 3.513 15.302 3.496 15.216 C 3.432 14.905 3.308 14.616 3.153 14.341 C 2.85 13.802 2.426 13.371 1.941 12.998 C 1.897 12.964 1.843 12.938 1.791 12.92 C 1.627 12.861 1.468 12.919 1.383 13.071 C 1.349 13.131 1.323 13.2 1.313 13.268 C 1.271 13.585 1.313 13.894 1.47 14.173 C 1.636 14.469 1.821 14.755 1.998 15.044 C 2.114 15.234 2.228 15.426 2.349 15.613 C 2.46 15.785 2.611 15.912 2.819 15.941 C 2.967 15.962 3.118 15.956 3.265 15.916 C 3.4 15.879 3.481 15.788 3.508 15.651 C 3.519 15.595 3.52 15.538 3.527 15.473 Z M 0.002 6.208 C 0.012 6.137 0.023 6.066 0.032 5.995 C 0.085 5.619 0.213 5.27 0.403 4.941 C 0.663 4.493 1.005 4.12 1.422 3.815 C 1.491 3.765 1.555 3.709 1.627 3.663 C 1.668 3.637 1.718 3.62 1.765 3.614 C 1.831 3.606 1.899 3.613 1.972 3.613 C 1.966 3.724 1.993 3.842 1.93 3.953 C 1.481 4.749 1.033 5.545 0.585 6.341 C 0.522 6.453 0.434 6.541 0.33 6.613 C 0.209 6.698 0.099 6.663 0.056 6.522 C 0.032 6.446 0.026 6.366 0.013 6.286 C 0.009 6.263 0.005 6.24 0 6.218 L 0 6.208 Z M 19.654 7.408 C 19.638 7.496 19.626 7.604 19.6 7.706 C 19.572 7.813 19.48 7.837 19.394 7.767 C 19.288 7.68 19.195 7.58 19.126 7.458 C 18.561 6.456 17.994 5.456 17.427 4.455 C 17.342 4.304 17.302 4.138 17.276 3.969 C 17.257 3.846 17.346 3.779 17.466 3.823 C 17.626 3.883 17.773 3.969 17.907 4.078 C 18.359 4.442 18.709 4.895 18.991 5.402 C 19.226 5.824 19.427 6.261 19.546 6.731 C 19.573 6.84 19.595 6.95 19.613 7.061 C 19.63 7.17 19.639 7.28 19.654 7.409 Z M 10.557 0.546 L 9.405 0.546 C 9.325 0.546 9.245 0.542 9.165 0.537 C 9.112 0.533 9.064 0.515 9.031 0.469 C 8.993 0.418 8.994 0.375 9.037 0.329 C 9.109 0.251 9.196 0.195 9.296 0.162 C 9.558 0.076 9.827 0.023 10.103 0.006 C 10.598 -0.024 11.073 0.065 11.533 0.241 C 11.608 0.269 11.672 0.324 11.739 0.372 C 11.753 0.382 11.756 0.418 11.75 0.439 C 11.746 0.453 11.722 0.471 11.704 0.474 C 11.519 0.495 11.334 0.52 11.148 0.529 C 10.951 0.539 10.754 0.531 10.557 0.531 L 10.557 0.547 Z" fill="rgb(101, 21, 229)" height="19.654427367156625px" id="w1pEMZlVs" transform="translate(0 0)" width="19.721078229664776px"/></g></svg>)

Beyond Connectivity: The Mandatory Shift to Enterprise Revenue

With consumer ARPU flatlining and connectivity heavily commoditized, the future of telco profitability lies in the enterprise sector. Discover why moving "up the stack" with revenue-ready edge cloud services is no longer optional, but mandatory for capturing the $400 billion B2B opportunity.

Swarmio Team

Technical Analyst

Table of contents

Share

Beyond Connectivity: The Mandatory Shift to Enterprise Revenue

Executive Summary:

Consumer connectivity no longer drives growth; core B2C revenues have flatlined, and traditional business models are structurally broken.

A massive $400 billion enterprise (B2B) market has emerged, driven by accelerating demand for low-latency, localized edge computing applications like real-time AI and gaming.

Growth now comes from platforms and services, not access alone; telcos must move up the stack to avoid being relegated to low-margin utility providers.

By deploying a monetization layer like Swarmio Core, telcos can convert their dormant, underutilized infrastructure into high-margin, revenue-ready edge cloud products in weeks, not years.

1. The Strategic Crossroad: The End of the Connectivity Monopoly

The global telecommunications industry is navigating one of the most precarious and consequential strategic transitions in its history. For over a century, the fundamental business model of the telecom operator was virtually unassailable: lay the physical network, acquire the subscriber, and charge a premium for access. This model funded the massive capital expenditures required to wire the globe, build cellular towers, and usher in the mobile revolution. However, as we look toward the second half of the 2020s, that paradigm has irrevocably shifted.

The very connectivity that operators spent billions to deploy has become the victim of its own success. It is now a ubiquitous, expected, and heavily commoditized utility. In boardrooms across the globe, C-suite telecom executives are confronting a stark realization: the telco revenue model is structurally broken.

The core products that historically drove massive profitability—voice, messaging, and data—are now low-margin commodities with little pricing power. The industry finds itself trapped in a cycle of relentless capital expenditure, required to fund the rollout of 5G Standalone (SA) and deep fiber networks, while the top-line revenue generated by these networks remains stubbornly flat. The era of relying on basic access fees as the primary engine of corporate growth is officially over. Moving forward, enterprise revenue is now mandatory.

2. The Consumer Plateau: Why B2C Can No Longer Sustain the Industry

To fully grasp the urgency of this pivot, one must examine the sobering data emerging from the business-to-consumer (B2C) segment. The consumer market, once the undisputed cash cow of the telecom world, has reached a state of profound saturation. Core revenues have flatlined. ARPU growth has stalled globally, while operating costs continue to rise.

According to the comprehensive PwC Global Telecom Outlook, the willingness of consumers to pay for connectivity is flat-to-down. Despite the fact that global data consumption over telecom networks is expected to nearly triple by 2027—driven largely by high-bandwidth digitized video and social media consumption—this surge in traffic is not translating into a proportionate surge in revenue. In fact, PwC projects that global mobile Average Revenue Per User (ARPU) will actually tick down marginally to $6.20 in 2029, a decrease from $6.32 in 2024. Telcos are carrying exponentially more data for the exact same, or slightly less, money. Consumer connectivity no longer drives growth.

This stagnation is heavily echoed by insights from KPMG's "Telco to Techco" analysis. KPMG reveals that while the broader technology sector has enjoyed explosive expansion, telecom service revenues have languished with a compound annual growth rate (CAGR) of just under 1 percent. In their assessment, KPMG forcefully concludes that telcos' traditional business models are no longer fit for purpose to address new digital opportunities.

The B2C market is characterized by hyper-competition, regulatory price caps in many jurisdictions, and an end-user base that views connectivity as a basic human right rather than a premium service. While consumer revenues will continue to provide a vital, massive base of cash flow to sustain legacy operations, they can no longer be the narrative presented to shareholders for future growth. The path forward necessitates looking elsewhere, specifically toward the complex, high-value needs of the modern enterprise.

3. The $400 Billion Enterprise Lifeline

If the consumer market represents a plateau, the enterprise (B2B) sector represents a soaring mountain of untapped potential. However, simply shifting sales teams to target corporate clients with traditional connectivity packages is a deeply flawed strategy. The nature of enterprise demand has fundamentally changed, and operators must adapt their offerings accordingly.

Research from GSMA Intelligence has quantified this shift, identifying a staggering $400 billion addressable market for telcos in B2B technology services by 2030. This opportunity equates to approximately 35% of the existing mobile operator revenue base worldwide, providing a definitive lifeline for an industry in desperate need of a growth catalyst.

Yet, the GSMA report contains a critical caveat: telcos must look far beyond connectivity-driven solutions. Currently, core telecom B2B services—such as SD-WAN, unified communications, and standard mobile voice and data—contribute around 70% of operators' B2B revenues. However, these legacy services offer virtually no headroom for expansion, with a projected CAGR of just 3% through 2030.

In stark contrast, enterprise spending on advanced technology services—including cloud computing, edge networks, cybersecurity, and artificial intelligence—is exploding. This advanced tech market was valued at over $1.16 trillion in 2023 and is expected to grow at a robust 14% CAGR. To capture a meaningful share of this market, telcos must move up the stack. Growth now comes from platforms and services, not access alone.

Enterprises in sectors like manufacturing, financial services, and automotive are undergoing massive digital transformations. They are investing heavily in advanced connectivity, IoT, and AI technologies to bolster operational efficiency and agility. These innovations are generating massive data volumes that require localized, highly secure processing environments. They do not just need a pipeline to the internet; they need a localized digital ecosystem. Enterprise demand is accelerating.

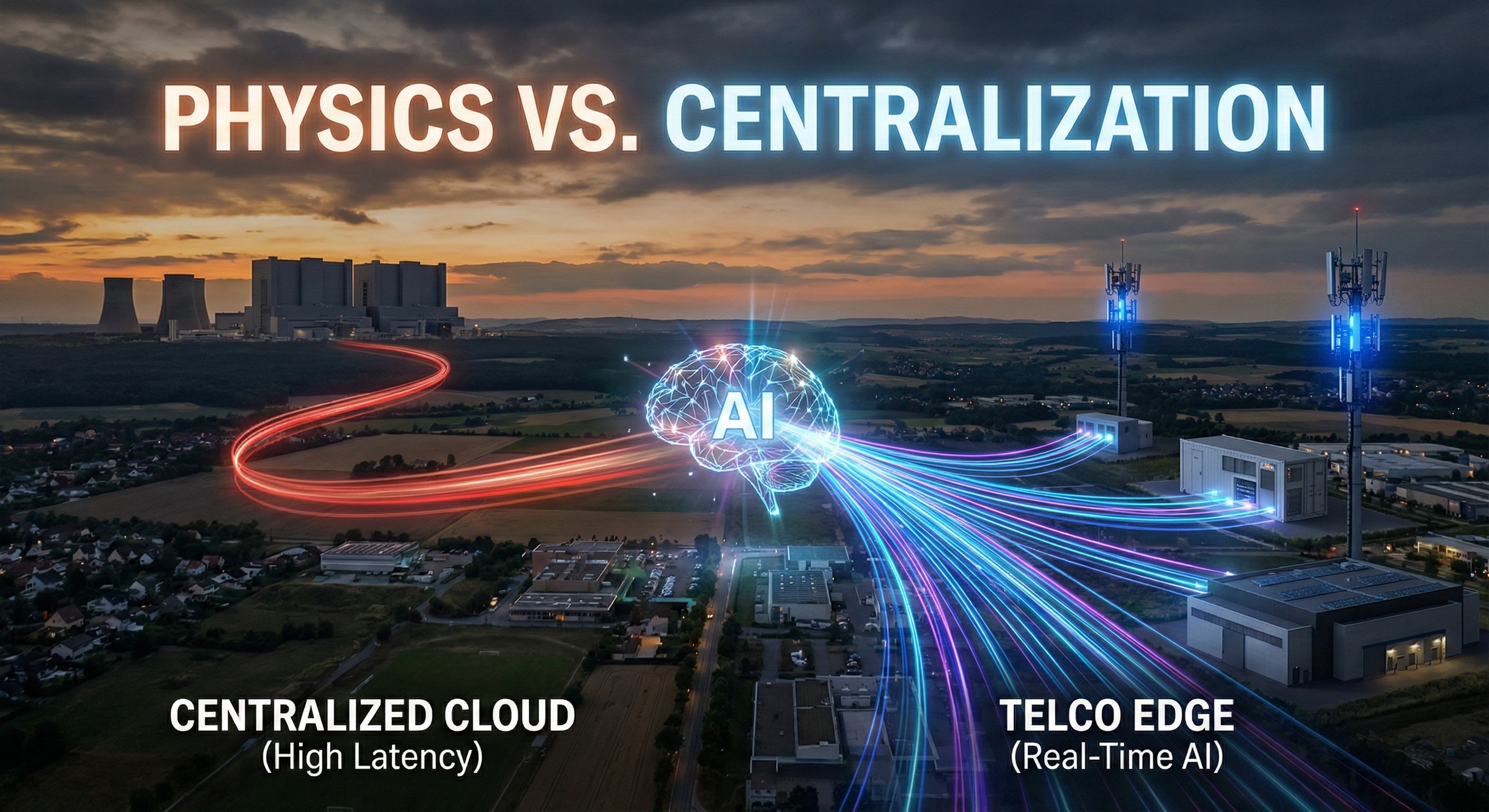

4. The Physics of Enterprise Demand and the Edge Advantage

The catalyst for this shift in enterprise spending is rooted in the physical requirements of next-generation applications. AI, gaming, fintech, and real-time applications require low-latency, local execution.

For the past decade, enterprises happily migrated their workloads to centralized public clouds operated by hyperscalers like AWS, Google Cloud, and Microsoft Azure. But the centralized model is now showing its physical and geographical limitations. When a robotic arm on an assembly line utilizes computer vision to detect microscopic defects, or when an autonomous vehicle relies on AI to navigate a complex intersection, sending data to a centralized data center hundreds of miles away introduces unacceptable delays.

Furthermore, stringent data sovereignty regulations are forcing enterprises, particularly in finance, government, and healthcare, to process and store data strictly within their own national or regional borders. Centralized clouds, by their nature, struggle to meet these localized requirements efficiently and economically.

This is where the telecom industry holds an asymmetrical advantage. Telcos have already invested heavily in data centers, MEC, and edge computing. They possess the distributed real estate, the power infrastructure, and the localized fiber networks necessary to bring cloud computing directly to the enterprise's doorstep. They have the trusted brands, regulatory approvals, and established billing relationships with millions of corporate customers. In theory, telcos are perfectly positioned to win at the edge.

5. The Monetization Gap and the Software Abstraction Imperative

Despite this inherent advantage, the reality on the ground is less triumphant. The telecom industry is suffering from a profound monetization gap. While the physical assets are in place, billions in stranded infrastructure exist across the globe. Much of this capacity remains underutilized, generating little or no return.

Why are these assets sitting idle while enterprise demand skyrockets? The answer lies in the absence of a software abstraction layer. Demand has shifted, but telcos can't capture it. Telcos lack the speed, tooling, and product frameworks to monetize this demand.

Having an empty rack in a Multi-access Edge Computing (MEC) facility does not make a telco a cloud provider. Enterprise developers demand the frictionless, automated, API-driven experience they receive from hyperscalers. When they attempt to deploy workloads on telco edge infrastructure, they are often met with fragmented systems, manual provisioning processes, and a lack of unified orchestration. Without a monetization layer, the telco edge remains a cost center, not a growth engine. Infrastructure exists, but revenue requires transformation.

This sentiment is echoed by recent analysis from McKinsey & Company, which notes a significant inflection point in the technology sector: enterprise spending is shifting from pure infrastructure development toward the software that allows organizations to monetize that infrastructure. For telcos, building the MEC node was only step one; deploying the software to productize it is the critical, mandatory step two.

6. Productizing the Telco Edge with Swarmio Core

To transition from a provider of raw infrastructure to a purveyor of high-margin edge cloud services, telcos must adopt a new operating paradigm. They require a unified system that bridges the gap between their physical assets and the enterprise developer.

This is the exact purpose of platforms like Swarmio. Swarmio acts as the operating system that productizes the telco edge. It provides a simple, repeatable model that turns telco assets into sellable edge cloud products.

The architecture of this transformation is built on a structured, three-layer approach:

Layer 1: Telco Assets: This represents the foundational layer where the infrastructure already exists. It includes edge and MEC locations, regional data centers, network infrastructure, bare metal, and public/private cloud resources.

Layer 2: Swarmio Core: This is the critical software abstraction layer. Swarmio Core converts infrastructure into products. It acts as the unified control and monetization layer for the telco edge. It provides zero-touch orchestration, automating deployment and operations across heterogeneous infrastructure. Crucially, pricing, policy, and usage are embedded in the platform, ensuring built-in monetization.

Layer 3: Revenue-Ready Solutions: Once the core is established, the telco can deploy specific industry verticals. These are packaged, priced, and ready to be sold by telcos. By utilizing this platform, telcos can launch new edge cloud services in weeks, not years.

7. Activating High-Margin Verticals without Capital Drag

One of the most significant advantages of this operating system approach is massive capital efficiency. Historically, if a telco wanted to launch a new product vertical, it required a massive, bespoke IT build, complete with new hardware, siloed software systems, and heavy systems integration.

With a unified platform, expansion becomes frictionless. Swarmio expands into new verticals on a single Core. Every vertical runs on the same Swarmio Core—no re-architecture, no platform sprawl. A single Swarmio Core deployment supports multiple sites and verticals, enabling growth without rebuilding platforms or increasing operational complexity.

This allows telcos to rapidly attack the most lucrative segments of the $400 billion enterprise market through a partner-led vertical expansion. Partners bring domain expertise and customers; Swarmio delivers the orchestration, automation, and monetization layer, enabling fast, capital-efficient expansion.

For example, Sovereign AI is becoming a massive requirement for governments and enterprises. Swarmio AI turns telco edge infrastructure into sovereign, low-latency AI services for enterprises and governments. The telco can offer fully managed AI inference on telco-edge GPUs, ensuring the workloads remain data-resident and compliant by design.

Similarly, the platform enables the deployment of Swarmio Gaming, a revenue-generating, latency-critical vertical built on Swarmio Core. Telcos can offer Game Server Hosting as a Service to B2B game publishers, providing low-latency game hosting on the telco edge, fully managed.

8. The New Commercial Reality: Usage-Based Growth

Ultimately, the transition "up the stack" is about rewriting the telecom financial model. The industry must break free from the constraints of static, flat-rate monthly subscriptions that fail to capture the true value of the network.

By deploying a monetization layer, telcos unlock a telco-native commercial model designed for predictable expansion and long-term scale. This model is structured around a combination of fixed recurring revenues and variable upside.

The foundation is built on Swarmio Core Access Fees, which provide mandatory platform access per telco group, and Site Enablement Fees, which scale by deployed sites and edge locations. This creates a stable baseline.

However, the true exponential growth engine lies in Usage-Based Fees. Revenue is generated by consumption, with variable revenue tied to solution-specific usage such as compute, inference, transactions, or workload metrics. This ensures that as an enterprise customer scales their AI models, or a game publisher sees a spike in player concurrency, the telco's revenue grows naturally as demand increases. This is the exact financial mechanism that propelled the hyperscalers to trillion-dollar valuations, and it is now available at the telco edge.

9. A Repeatable Blueprint: Land, Expand, Scale

The commercial rollout of this enterprise strategy relies on a repeatable expansion model designed for telco group deployments.

LAND: The journey begins with an initial deployment with a single operator. It involves launching one revenue-ready solution across limited sites or regions, allowing for fast validation of performance and monetization. The goal is to prove value inside one operating unit.

EXPAND: Once validated, operators can go deeper inside the same telco group. This phase involves activating additional solutions on the same Swarmio Core and rolling out across more edge sites and regions. This strategy increases revenue per telco without replatforming and maximizes value within one telco relationship.

SCALE: Finally, operators replicate across the telco group footprint. By extending deployments to other countries and operating companies, the telco can reuse the same platform, processes, and commercial model. This turns one telco win into a multi-region platform rollout.

Conclusion: The Mandatory Evolution

The era of the pure-play connectivity provider is drawing to a close. The market has spoken: consumer connectivity is a necessary utility, but enterprise edge computing is the premium growth engine of the future. The telecommunications industry stands before a $400 billion opportunity, armed with the precise physical infrastructure required to capture it.

To bridge the gap between dormant assets and enterprise demand, telcos must adopt the mindset of a technology company. They must deploy the software abstraction layers necessary to productize their edge, automate their orchestration, and monetize their capacity on a granular, usage-based level. The infrastructure advantage is real, but it must be activated. For the modern telco, moving up the stack is no longer an ambitious goal; it is a fundamental requirement for survival and future prosperity.

References & Further Reading:

Market Intelligence: GSMA Intelligence: Telcos eye $400bn enterprise opportunity

Industry Strategy: McKinsey & Company: Technology, media, and telecommunications M&A outlook

Telecom Projections: PwC: Perspectives from the Global Telecom Outlook 2025–2029

Business Model Evolution: KPMG: Telco to Techco